Strong Q1 of 2025 by The Cigna Group

Really strong showing by Evernorth drives top line from specialty drugs!

Sponsored by Dave Breininger at Talent Wave

Talent Wave is transforming how healthcare organizations discover and retain top-tier talent. Led by industry specialist David Breininger, Talent Wave connects exceptional individuals with visionary healthcare companies through a personalized, innovative approach. . Learn more at www.talentwaveassociates.com. Contact David at (567) 304-3102 or DBreininger@talentwaveassociates.com

The Cigna Group was the final of the “Big Six Payors” to report earnings last Friday (5/2/25) and I had a chance to dig through the 10Q and earnings transcript. The stock is down 3% since the report but it was a great quarter as they grew top line 14% to over 65 billion in the quarter while also driving a higher EPS of $6.74. David Cordani (CEO) took some time in the call to introduce the new COO (Brian Evanko) and new CFO Ann Dennison. I continue to be a fan of the company as they have divested the non-core assets (Medicare Advantage) and have leaned into dominating the commercial/employer space along with providing services to these same customers. Overall, they slowed the downside risk from the stop-loss policies and are showing strong growth in specialty drugs along with the Express Scripts/PBM space. They increased guidance on their EPS to $29.60 and had a really strong call so I look for them to have a great 2025. Below were some of the things that stood out to me from the earnings call.

Cigna (Health Benefits)

Currently represents about 40% of the companies revenue and a huge partnership mechanism as about 94% of the business is with employer groups providing benefits for their employees. I believe this has been a great flywheel for them as they get close with these employers and then build valuable solutions for HR/benefits teams that usually fit under the Evernorth umbrella. As I have said in the past, Amazon is a business built around high spending retail customers while Cigna is doing the same wrapping themselves around the employer/broker customers.

During the call, they addressed some of their stop loss business which caused them some downside risk last year and said that it is tracking on schedule with projections which is positive. Also, said they had 9% revenue growth in the health benefits business and have done really well in the Select 500 employer (small to medium size employers) market in the 2026 selling season. They have begun to reprice some of their stop-loss business this year as they look to get some margin back on this employer insurance model where Cigna bears more risk. They see 2025 and 2026 as years to move up their premiums but do not expect to see fall off as they have quite a few levers to help employers (PBM, Evernorth, etc.).

Evernorth

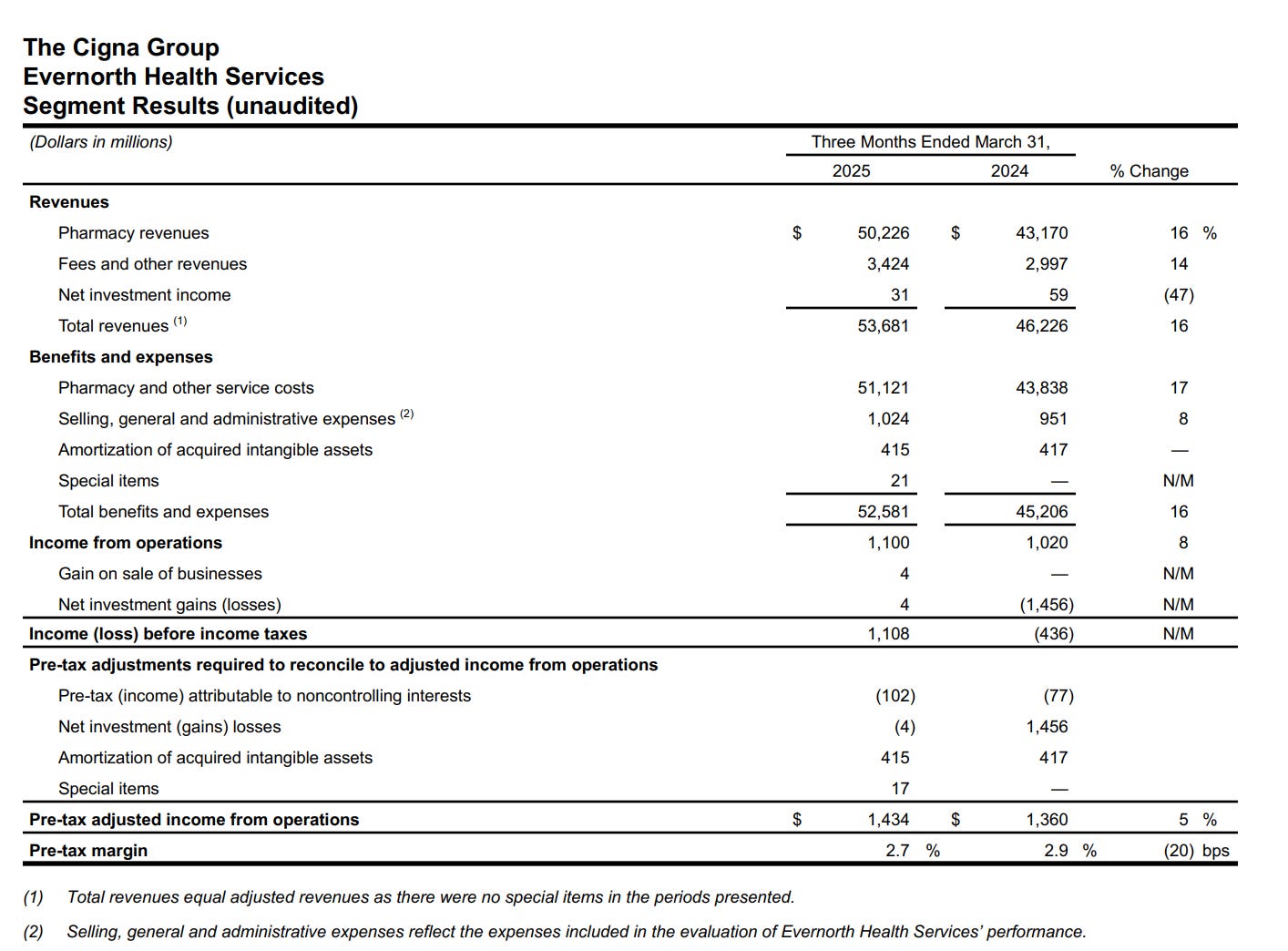

Continues to be the growth driver of top line revenue and is currently 30% of the company's revenue. As you will read further down, specialty and biosimilar drugs are driving revenue and the stack of assets that Cigna/Evernorth has built in this area is strong and well poised for future growth with the specialty drug explosion and some of the fuel provided to specialty drugs by the Inflation Reduction Act cap of out of pocket expenses.

Evernorth Specialty and Care Services

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.