Q1 2025 Review: The Big Six Payors — Winners, Losers, and the Road to Q2

The Healthcare Economy

All of the “Big Six Payors” finished up earnings a couple of weeks ago, and I figured I’d force-rank each of them to give everyone a framework for the key storylines headed into Q2 earnings in July. For context, my rankings aren’t based purely on earnings beats or stock performance, they reflect execution, strategic clarity, and how well each organization is positioned going forward. Additionally, I have handicapped some of the companies based on legislative headwinds or potential liability in the latter half of the year.

Cigna (#1)

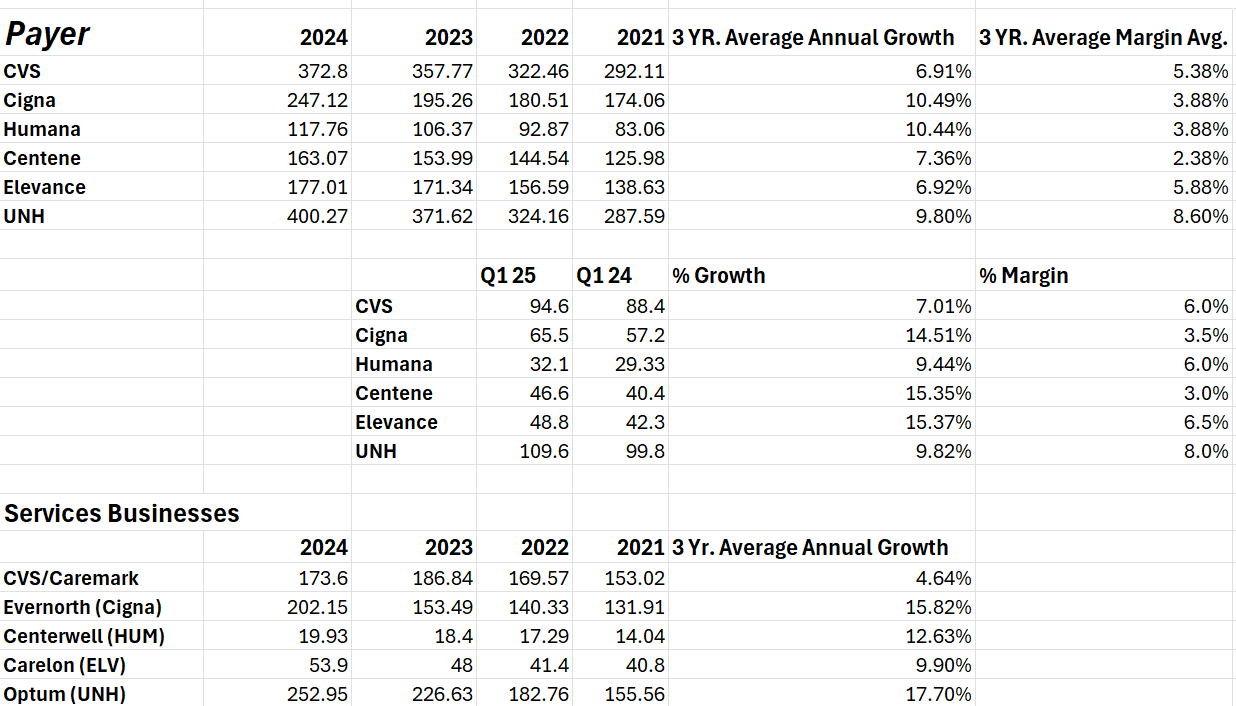

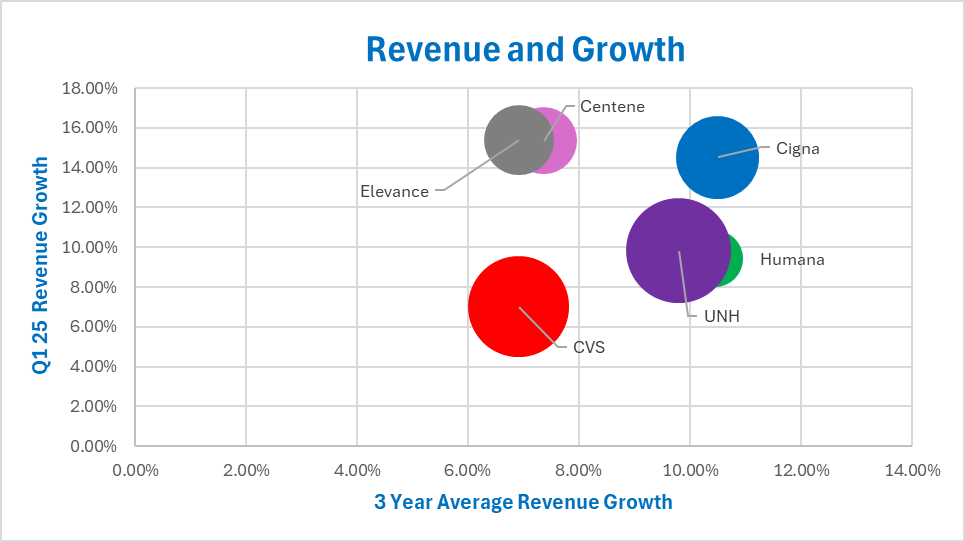

Cigna tops my list this quarter as the only one in the Big Six not weighed down by government lines of business. While others navigated Medicare Advantage pressure or Medicaid redeterminations over the past two years, Cigna doubled down on the commercial employer market and it’s working. Revenue grew 14% to $65 billion, EPS hit $6.74, and guidance rose to $29.60. The Health Benefits segment, now 40% of revenue, saw 9% growth, boosted by strong stop-loss repricing and employer momentum.

Sponsored by Dave Breininger at Talent Wave

Talent Wave is transforming how healthcare organizations discover and retain top-tier talent. Led by industry specialist David Breininger, Talent Wave connects exceptional individuals with visionary healthcare companies through a personalized, innovative approach. . Learn more at www.talentwaveassociates.com. Contact David at (567) 304-3102 or DBreininger@talentwaveassociates.com

Meanwhile, Evernorth continues to shine, especially in specialty pharmacy and biosimilars markets which are becoming a battleground for CVS, Cigna, and UNH. One of the developing services under Carelon is EncircleRx which now covers 9 million members for GLP-1 coverage which is a top concern for domestic employers. Last week, they announced a $200 GLP-1 out-of-pocket cap to give their customers additional value as they look to give access to these weight loss/diabetes drugs to their employees while managing risk. Express Scripts also saw 14% growth, which is impressive given they had such a great 2024 with the addition of Centene. Cigna’s strategic clarity, employer-first execution, and strong tailwinds in specialty and pharmacy pushed them clearly to the top for Q1.

CVS Health (#2)

If you told me a year ago I’d have CVS in the second spot, I’d have laughed. But under new CEO David Joyner, they’re trimming non-core segments (like MSSP and ACA) and re-centering around their strengths. CVS posted nearly $95 billion in revenue (up 7%) and grew EPS from $1.31 to $2.25. They’re projecting 600,000 new Aetna members this year and saw sharp improvements in medical benefit ratio, especially in Medicare Advantage.

The GLP-1 strategy is aggressive and smart as Wegovy will be preferred on July 1, paired with their weight management program and in-person pharmacy access at 9,000 CVS locations. Look for the GLP-1 battle with Carelon/Encircle as they all look to build a solution with proper cost containment for employer customers. On the PCP front, Oak Street continues to scale (+37% at-risk members), and CVS has become the top-ranked chain for medication adherence. CVS is becoming a leaner, better-aligned health services company. This was a high-clarity, high-discipline quarter that earned them the #2 spot which has me in disbelief.

Elevance (#3)

Elevance had a solid Q1 and takes the third spot of the rankings. Revenue rose 15% versus Q1 of last year, with strong Medicare Advantage retention, 11% ACA growth, and solid Medicaid footing. Membership rose by 99,000 and, notably, they sidestepped the MA utilization spikes that crushed UNH and Humana during the quarter. While operating margin dipped due to Medicaid costs, early rate alignment talks show promise for a more stable second half for Elevance.

The real engine here is Carelon, Elevance’s services arm, which saw 38% revenue growth. Their acquisitions of CareBridge, Kroger Specialty, and Paragon are beginning to scale, and CarelonRx is quietly building PBM momentum among Blues and employer partners. With CVS exiting ACA and Elevance growing it, plus STAR stability and execution discipline, they’re well-positioned heading into 2026, especially if they can leverage Carelon services across more risk-bearing models.

Humana (#4)

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.