Humana's Hard Reset: Building for Value as America Ages

Q3 2025 Earnings For Humana

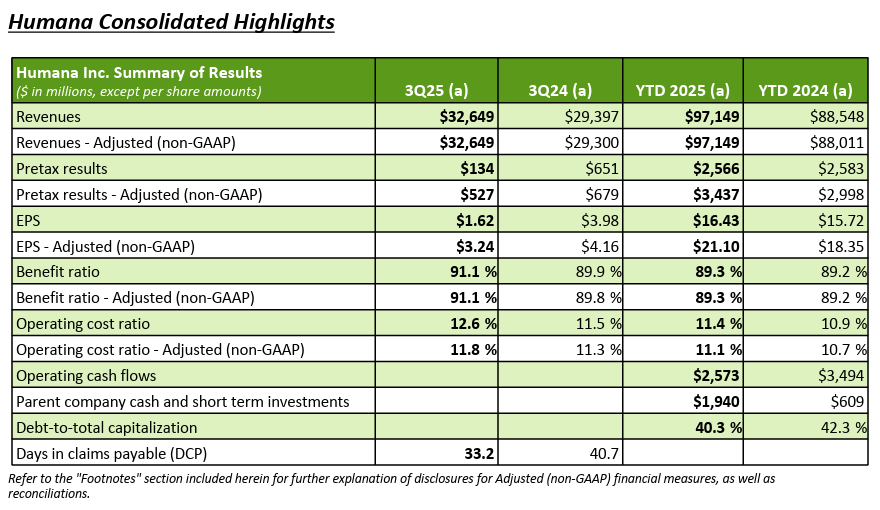

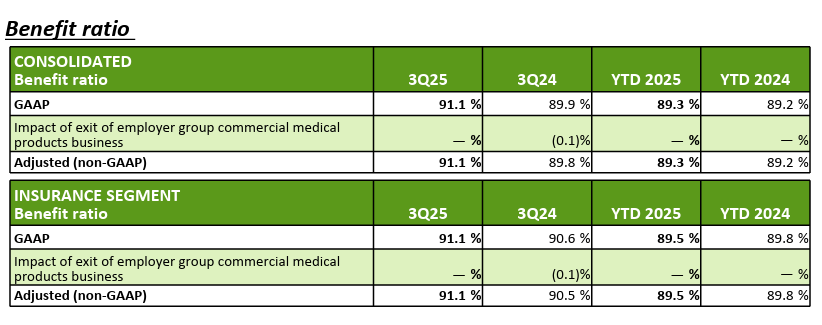

Humana was the last of the “Big Six Payors” to report earnings last Wednesday before the market opened and the stock has fallen 13.5% as the market did not like the continued headwinds in their core business of Medicare Advantage. Revenue was up 11.4% for the quarter and 10% through the first 9 months of the year. I think the concern was the 120 basis point increase in benefit ratio and the EPS falling 22% over the same quarter last year. Overall, not a lot has changed and after reading the transcript along with the earnings, I feel like they are positioned for a recovery as they shift more into Jim Rechtin’s new strategy of long term thinking, customer acquisition cost, customer lifetime value and churn. This fits well in value based care as we have read from other payers but also clinical data which shows that keeping a patient consistently along with engagement will drive better outcomes at a lower price. Wall Street did not like the quarter but I liked the earnings call and feel that they will reap rewards.

Medicare

Open enrollment is going well and they are performing to the higher end of their expectations a few weeks in. Additionally, their direct channel is producing nice volume but also a high quality member that they feel has a great lifetime value for them. They did not give a sales goal on this call as he said they are going to be picky as new members roll in to make sure the underwriting for 2026 is going to track with their modeling. Jim Rechtin went on to say that the number of new enrollments is not the internal KPI that they are tracking but more around the quality of the members ingested. They feel like their customer service focus is getting them really strong retention early on in the AEP process.

David Dintenfass was on the call and is shifting them towards the Peter Fader from Wharton line of thinking on Customer Centricity. Rather than chasing aggressive membership gains, the company is prioritizing lifetime value, net present value, and retention across its book of business. They described a shift toward balanced pricing that aligns with risk, ensuring that every plan contributes sustainably over time rather than relying on short-term enrollment spikes from low-margin products. After two years of benefit reductions and market exits, Humana is now focused on stabilizing its product portfolio and providing consistency for members, particularly in core medical benefits. The company believes this stability, combined with strong underwriting collaboration and a customer-first mindset, will drive both margin recovery and retention improvement in 2026. Ultimately, management made clear that growth will be pursued only where it supports long-term profitability, member satisfaction, and operational excellence. This has been a strategy that Google and many others have adopted over the past decade since Amazon has really focused on acquiring the most valuable customers in each vertical. This is not a typical thing in healthcare but it sounds like they are moving towards customer acquisition cost, lifetime and churn as internal metrics they will be focused on in the next several quarters.

Sounded like they are moving towards a diversification strategy as a deliberate move to reduce concentration risk within its Medicare Advantage portfolio for STAR ratings. For several years, nearly half of its membership has been tied to a single contract known as 5216, creating outsized exposure if that contract underperformed. The company is now working to spread its members more evenly across multiple contracts to build a more stable and resilient portfolio. As part of this approach, Humana is shifting more members into contracts rated 4 to 4.5 stars to strengthen overall quality and revenue stability. They noted that this process will take multiple product cycles to complete, but the company has already made meaningful progress and expects continued improvement over the next few years.

They reiterated that they are on track with the 2028 plan outlined at Investor Day but emphasized it is too early to provide formal 2026 guidance given the ongoing Annual Enrollment Period (2% margin range). The company expects margins for new Medicare Advantage members to vary depending on which contracts they are enrolled under, with members tied to 4 or 4.5-star contracts generating higher profitability. Overall, they anticipate its individual Medicare Advantage margins, excluding the impact of Stars, to roughly double in 2026 compared to 2025, supported by better product design, channel mix, and pricing discipline. On quality performance, management highlighted that operational improvements this year have produced broad progress across key HEDIS and patient safety measures, and they remain confident that these gains will position Humana well as it works through the next wave of CAHPS and HOS metrics in early 2026.

Part D

Humana discussed several steps it has taken to manage challenges in its Medicare Part D business stemming from the Inflation Reduction Act (IRA). The company decided to take back more Part D risk after the IRA significantly shifted costs, while also reducing benefits over the past two years to ensure products remain financially sound and attractive for both Humana and its value-based care partners. In addition, Humana has implemented Stars mitigation programs designed to offset revenue impacts tied to lower quality ratings, depending on performance outcomes. Management noted that they are actively working with their value-based partners to adjust contracts and navigate these headwinds, expressing confidence that the combination of these actions positions them well for stability and growth in the coming years.

They are seeing strong momentum, particularly within the basic and value plans. They are now below the benchmark in roughly twice as many states as last year, positioning themselves to capture more auto-enrolled low-income subsidy members and pick up competitor reassignments. They feel it strengthens the company’s Part D book with stable, predictable growth in 2026.

Medicaid/Duals

They spent some time emphasizing its growing focus on dual-eligible and Medicaid populations, viewing these segments as important drivers of both growth and margin expansion. They are prioritizing Medicaid opportunities that align closely with dual-integration markets, where it can leverage its strong position in Medicare Advantage to deepen relationships with high-value members. Dual-eligible products typically deliver stronger first-year margins than traditional Medicare Advantage plans, providing a near-term financial lift while building long-term member retention for them. Looking ahead to 2026, they will expand into Michigan’s HIDE program and Illinois’ new dual market, with additional opportunities in South Carolina as that state moves to carve in dual-eligible beneficiaries. These expansions position them to grow its dual footprint and capture a larger share of this financially attractive and strategically important segment.

STAR Ratings Reaction

Humana addressed its Medicare STAR ratings with a tone of realism and measured optimism during the call. Jim Rechtin reiterated that while the company was disappointed by its bonus year 2027 results, the outcome was fully in line with internal expectations and prior guidance shared at its June investor conference. Importantly, Humana emphasized that operational improvements made late in 2024 have carried into 2025, creating positive momentum across nearly all quality metrics which set them up for a great 2028 STAR rating. The company highlighted that it has closed 600,000 more care gaps year over year, reflecting stronger member engagement, better preventive care outreach, and improved clinical coordination. Although they declined to speculate on final thresholds due to the curve-based nature of the STAR program, management expressed confidence in returning to top-quartile performance by bonus year 2028. They are focused on operational discipline and quality outcomes as key levers for restoring margin performance and competitive positioning in the Medicare Advantage market.

AI/Operational Improvements

One of the pillars of Jim Rechtin’s strategy since he began last year has been to drive operational efficiency. He highlighted significant progress in its operational efficiency initiatives, pointing to both technology adoption and strategic partnerships as key drivers. The company recently partnered with Genpact to outsource parts of its finance operations, a move designed to strengthen back-office capabilities while

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.