Elevance Q4 and Full Year 2024 Earnings

Beefing Up Carelon to Drive Revenue to Health Services

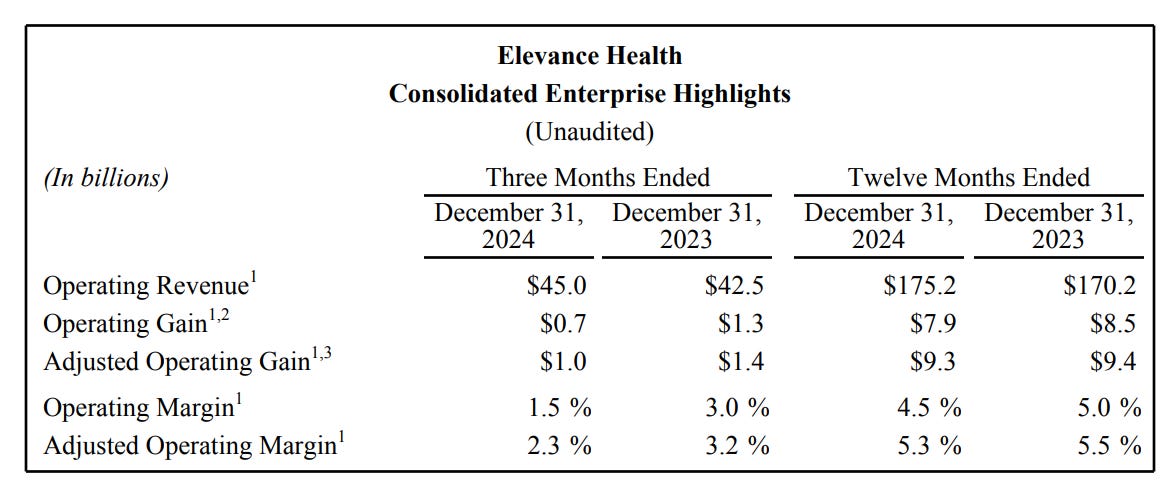

Overall, a really strong earnings call for Elevance as they reported before the market opened on Thursday. They were the second of the “Big Six Payors” to report after UNH, and overall, it is shaping up to be an average Q4 thus far. Elevance reported over 3% growth year-over-year, with top-line revenue exceeding $175 billion for the fiscal year. For the health insurance business, they lost 1.1 million members year-over-year, driven by Medicaid redeterminations as well as exiting some markets in the Medicare line of business that were no longer profitable. They noted that the higher revenue was attributed to higher reimbursement from state partners recognizing the elevated cost trends across the industry. They faced some margin headwinds, which were anticipated by investors expecting an elevated Medical Loss Ratio, leading to a year-over-year reduction in margins. The high note, in my opinion, was Carelon contributing to the revenue growth as they continue to acquire new companies while simultaneously winning customers in the Blue franchise. Below are the highlights for me after listening to the earnings call and reviewing the 10-K.

Medicaid This was the standout of the call as they beat Wall Street expectations for the Medical Loss Ratio in this line of business, although it remained elevated. They indicated that they aren’t fully aligned yet with states’ reimbursement levels but expect this to normalize in the back half of the year (likely by July). They highlighted savings generated through their complex care management programs, which include support from dedicated care teams and digital resources. These programs reduced inpatient admissions by 7%. Additionally, they noted an uptick in value-based agreements with providers compared to three years ago, with 35% of providers now taking downside risk (up from less than 20%). They expressed confidence in their ability to drive better care at a lower cost through Carelon platforms, which have been a cornerstone of their growth strategy.

Medical Loss Ratio MLR grew 320 basis points quarter over quarter but was less than anticipated by Wall Street which really saved the quarter for them. Year over year they grew 150 basis points in the MLR but expect this new level of elevation in expenses headed into 2025. Given this factor, they are seeking higher reimbursement from their State partners while simultaneously cutting their operating expenses to offset the increase in costs. This all had a profound impact on their EPS and operating cash flow took a large hit for 2024. They are hoping this is the high water mark for margin pressure on Medicare and Medicaid to be able to start to get back to normal margin profile in 2025 and 2026.

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.