CVS Q4 and Full Year 2024 Earnings

Nice Rebound For CVS as New CEO David Joyner Sets the Stage

CVS was the final of the “Big Six Payor” earnings to report last Wednesday before the market opened, and they managed to beat expectations, sending the stock up 20% over the past five trading days. It was a strong quarter as David Joyner kicked off his tenure as CEO after being appointed in mid-October 2024. For the year, CVS reported $372 billion in top-line revenue and successfully calmed the market's concerns about downside risks in their Medicare, ACA, and Medicaid business units. Some of the $1.1 billion reserve claim they put aside in Q3 helped smooth out the elevated MBR, as the health benefits division (Aetna) posted a $439 million loss in Q4. After going through the earnings transcript and the 10-K, here are the major highlights that I see as key drivers for their business in 2025.

PBM Legislation

In his opening remarks, Joyner defended the PBM model, emphasizing its role over the past three decades in preventing drug prices from climbing even higher. He pushed back against the narrative that PBMs are the problem, instead arguing that they keep drug manufacturers in check. He highlighted that branded manufacturers have already raised prices by $21 billion in 2025 alone and pointed out that manufacturers, not PBMs, are leading the charge to remove middlemen from the equation. Given Joyner's background at Caremark, it was interesting to see how he brought that perspective to CVS's broader business strategy. He also emphasized that PBMs have kept Part D drug price growth at just 1.8%, directly benefiting consumers. Additionally, he accused the FTC of “cherry-picking data points” in its arguments against PBMs.

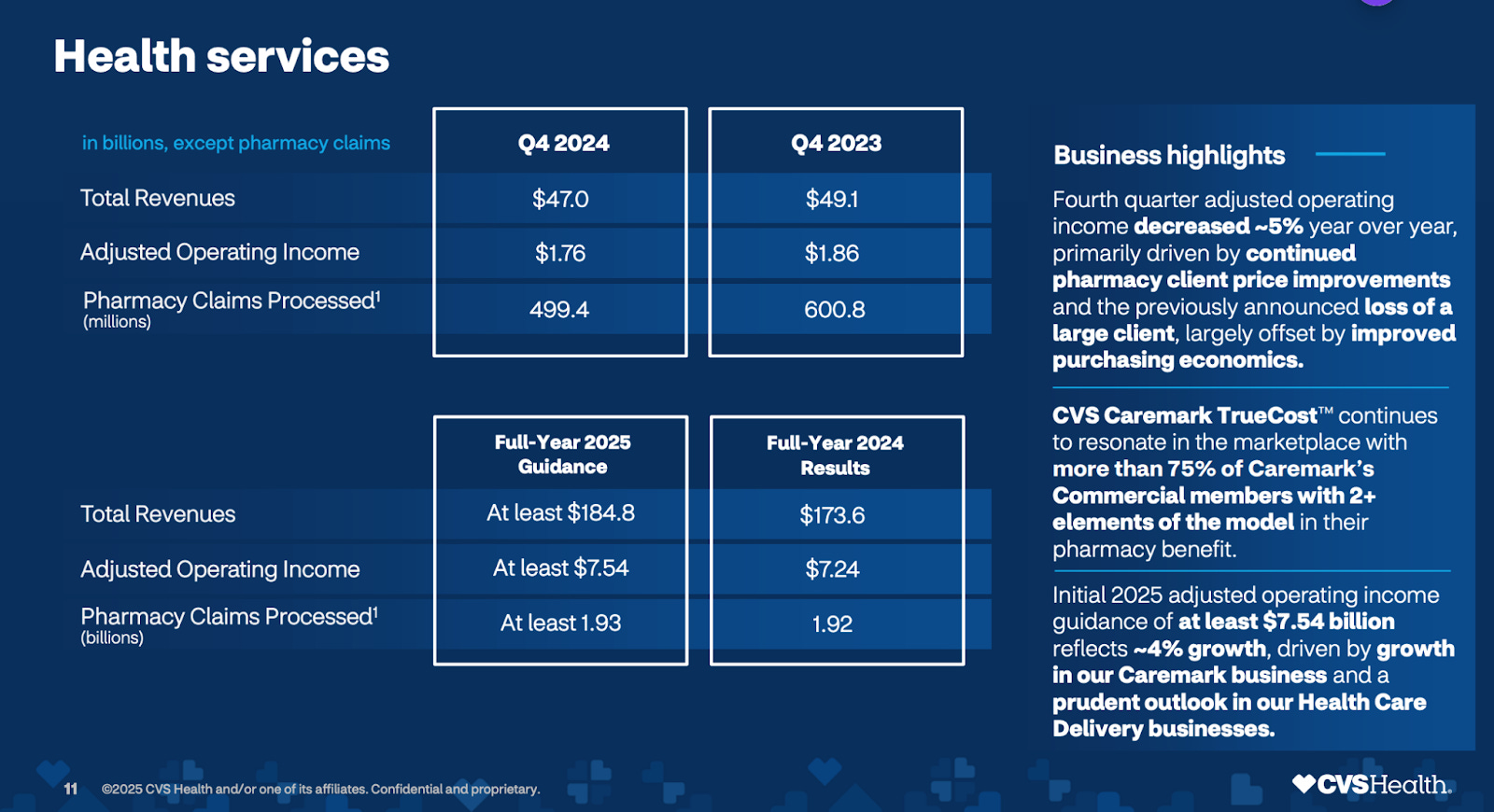

Caremark

Caremark is the nations largest PBM and had a rough year in terms of top-line revenue growth, largely due to the loss of the Centene contract. However, they have rebounded well, projecting a 4% increase in operating income for their health services business, reaching $7.54 billion in 2025. They are particularly optimistic about their TrueCost program, which will pass through 99% of rebates to clients, shifting away from spread pricing toward a fee-based model. The legislation and some of the negotiations on what some sort of regulations (if any) will look like will be the major theme for their PBM business as referenced above.

Cordavis/Biosimilars

Joyner highlighted CVS's aggressive push into biosimilars, stating that they had shifted 90% of their eligible book of business to a biosimilar priced 80% below branded Humira, with zero out-of-pocket costs for patients. This initiative alone generated over $1 billion in savings for customers. In the Q&A, Joyner expressed confidence that CVS is leading the industry in biosimilar conversions. This focus on biosimilars will be a key strategic area for PBMs over the next four years, as approximately $100 billion worth of specialty drugs go generic or have biosimilar equivalents coming to market. Big storyline to follow will be the announcement of their Stelara biosimilar equivalent availability this year as they look to run a similar play as Humira.

Oak Street/Signify

Karen Lynch's acquisitions of Oak Street ($10.6 billion in May 2023) and Signify ($8 billion in March 2023) remain a focal point for CVS. The company is continuing to integrate these assets into its broader healthcare ecosystem. Oak Street, a capitated primary care network, and Signify, a home healthcare provider, serve as key components in their Medicaid, Medicare, and dual-eligible strategy. In 2024, Signify conducted over 3 million home visits, while Oak Street grew value-based membership by more than 35% year-over-year. Key figures to follow will be the growth on the in-home visits by Signify and the number of payer agnostic contracts that Oak Street can pick up in 2025. Beyond that, you will want to follow the margins on these capitation agreements at Oak Street as many have struggled to make these profitable (OptumHealth).

Pharmacy and Consumer Wellness (Retail Pharmacy)

CVS reported record-high NPS scores for its pharmacy business, signaling strong customer satisfaction. They project 3.5% prescription growth in 2025, with revenue surpassing $134 billion (an 8% increase over 2024). However, operating income is expected to decline by 5% to $5.48 billion. As competitors scale down their retail footprints, CVS is well-positioned to capture additional market share.

Aetna (Health Care Benefits Unit)

Enrollment remained flat year-over-year, but revenue grew 23%, indicating higher reimbursement in key markets. However, CVS projects a decline of about 1 million members in 2025 from its current 27 million, with 800,000 of those losses coming from the ACA/Marketplace business. This reduction is driven by repricing efforts and government reporting headwinds on subsidies. Despite this, they expect top-line revenue of $132 billion in 2025, with operating income improving to $1.5 billion. The Medical Benefit Ratio (MBR) is expected to improve by 100 basis points to 91.5%.

Medicare Advantage

CVS expects high single-digit percentage losses in its Medicare Advantage book after pricing conservatively for 2025. Like its peers, it has also shrunk its footprint. However, they aim to restore margins to 3%-5% as the CMS rate increase exceeded 4% for the first time in three years. Elevated utilization and hospitalizations among seniors trended downward in Q4, leading to more optimistic projections for 2025. CVS is also factoring in the impact of the Two Midnight Rule, which drove up utilization in 2024. They ended 2024 with negative 4.5%-5% margins in their Medicare business, a major concern after Q1, but expect significant improvement in 2025 thanks to higher STAR ratings and stricter AEP pricing.

Medicaid

Approximately 40% of CVS's Medicaid state partners have adjusted reimbursement to reflect the acuity of their populations post-pandemic. Their medical affairs team has been proactive in securing early discussions with state partners, leading to an average reimbursement improvement of 4.5% across those agreements. While additional states will update their PMPM rates in July, CVS does not expect those increases to be as high as the current 4.5% average. This is going to be a nice tailwind for 2025 as the redeterminations are over, the acuity issues should subside in July and they should be in a strong position for margin expansion in 2026.

ACA

CVS ended 2024 with 1.85 million ACA members but expects enrollment to fall below 1 million due to pricing adjustments. The ACA business has been a drag on earnings, with $10 billion in premiums generating a $1 billion loss in 2024. CVS won’t have full visibility into the new member mix until March, when the first premium payments are collected. ACA has been such a boon for most payors as it has ballooned under the premium subsidies while also gaining some momentum in the commercial insurance space. I am going to be following how severely their numbers fall for enrollment in 2025 and keep track of their ability to recover to positive margins.

AI Initiatives

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.