CVS: From Expansion to Optimization

Highlights from the CVS Q3 earnings

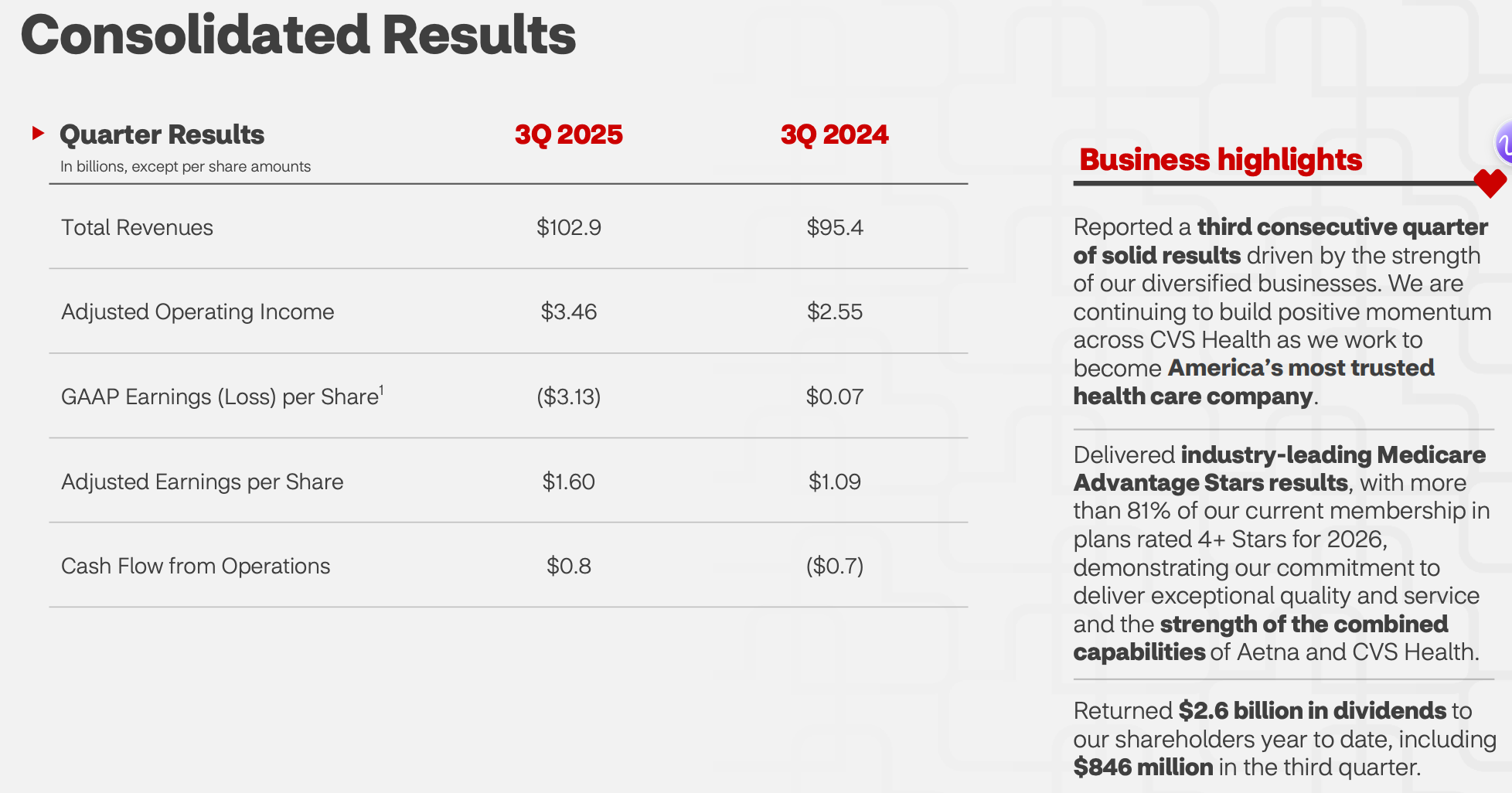

CVS reported earnings last Thursday (10/29) before the market opened and the stock slid about 8% as they recorded a 5.7 billion dollar impairment from the Oak Street acquisition from 2023. David Joyner is a year into his tenure at CVS after taking over October 17th of last year. He has done a great job bringing skeptical underwriting to the Aetna business to drive better bottom line results along with leaving the ACA line of business. The stock is up 23% since his tenure began and up 78% YTD so he has earned quite a bit of credibility in a year since joining.

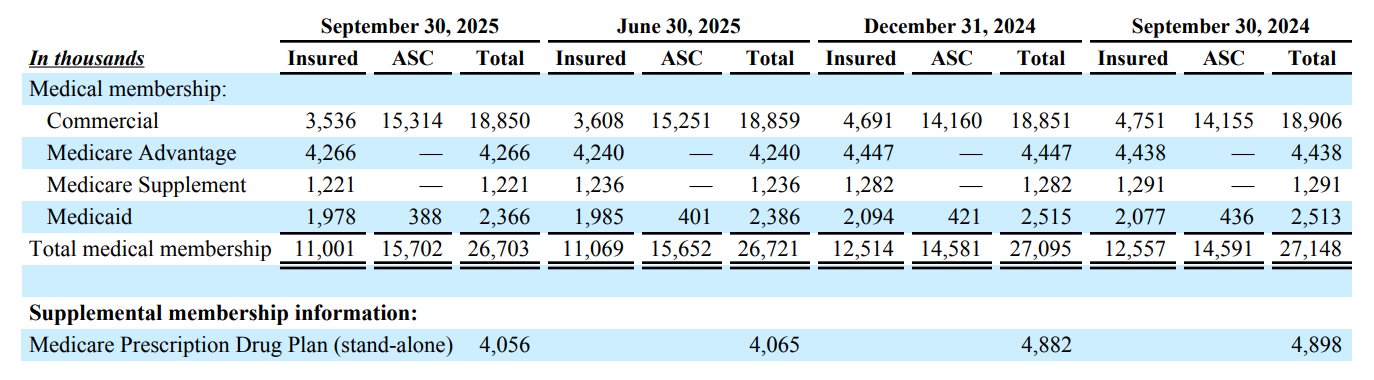

In the quarter, they topped 103 billion in revenue which is about 8% growth over last year. They had operating income of 3.5 billion which is about a 36% increase over 2024 as they have been able to skeptically underwrite much of the Aetna business which caused the stock crater in 2024. They closed the quarter at 26.7 million members in the Aetna business with about 445,000 member attrition since last year which was a part of their overall strategy under the new leadership. After reading through the earnings and looking at the 10-Q, below are my largest takeaways.

Aetna

Aetna’s medical benefit ratio improved to 92.8% in the third quarter, down from 95.2% a year ago, signaling stronger underlying performance across its government business and improved pricing discipline. This was to be expected given the immediate direction of David Joyner as he quickly shifted toward scrutinizing the underwriting. The decline was largely driven by favorable year-over-year impacts from premium deficiency reserves, positive prior period development, and continued operational progress in managing medical costs. Offsetting these gains were provider liabilities dating back to 2018 and worsening risk adjustment dynamics in the individual exchange segment, each contributing about 100 basis points to the ratio. Despite these headwinds, medical cost trends were modestly better than expected, particularly within Aetna’s individual Medicare Advantage book. Overall, the improvement in medical benefit ratio highlights effective cost containment and operational execution while acknowledging persistent pressures in risk adjustment and individual exchange acuity that remain areas of focus heading into 2026.

Medicare

They were really excited about the STAR ratings they received last month which moved them to 81% of their members in a 4 star or better plan and 63% of the members in a 4.5 star or better which is almost double the industry standard. They are early in the open enrollment process for 2026 but feel they are in a great spot with the geographies, the offerings and the underlying unit economics.

They highlighted disciplined execution in plan design, pricing, and footprint management, which has led to stronger-than-expected performance in the third quarter. Early signs from the current Annual Enrollment Period (AEP) suggest enrollment trends are tracking in line with expectations, and CVS expects to exit the period roughly flat in membership while maintaining margin improvement. Executives noted that the Medicare segment is benefiting from a more favorable cost trend environment and operational rigor, with repricing opportunities in group Medicare expected to support further gains in 2026. Overall, Aetna’s Medicare business is entering a multiyear recovery phase after 2024, positioning CVS to rebuild profitability and regain industry leadership through steady execution and a more rational approach to growth.

Commercial

The commercial business shifted to self funded and away from fully insured over the past year. Overall enrollment for Aetna remained flat (down 100K) in this line of business but the shift in the way the commercial/employer group is paying was interesting. With the company shifting out of the ACA, it will be interesting to see if this continues to shift lower for lower overall commercial enrollment. I would expect them to lean into traditional commercial (self funded) with Cigna as they have built quite a strong flywheel with traditional PBM, specialty pharmacy, retail pharmacy and inpatient specialty pharmacy as a way to help control costs. More often, we are seeing these as potential drivers (overall alignment) for employers when they are choosing the health benefits, pharmacy benefits and specialty benefits.

Medicaid

Small loss in enrollment, which is to be expected as the footprint nationally has shrunk from the high of 94 million beneficiaries in the US, to closer to 76 million today. With income verification along with other strings now being attached to Medicaid, I would expect them to also shrink stand alone Medicaid products. The focus under David Joyner has been better underwriting and given the lack of optionality in how the states pay, I would see Aetna moving more towards attacking the dual patients in order to ensure strong unit economics. Similar to commercial, the call did not include a lot of discussion on Medicaid and the majority was on the PBM, pharmacy and specialty pharmacy.

Caremark (PBM)

Caremark remains a critical driver of CVS Health’s overall enterprise earnings, even as the company faces some short-term headwinds from client contract renewals and pricing dynamics. They reiterated confidence in the PBM’s strategic direction, noting that a few recent contracts are temporarily affecting growth, but recontracting efforts are already underway to stabilize performance over the next several years. Despite this near-term drag, Caremark’s competitive positioning remains strong, supported by another successful selling season with nearly $6 billion in new client wins and retention rates in the high 90s. They had quite a few questions on the PBM during the Q&A given the fact they were projecting shrinking in the back of the year. They feel like the integrated pharmacy benefit services, cost management tools, and clinical expertise give them a strong message that resonated with clients during the selling season. Given their size as the largest US PBM (may be a toss with ESI) it is central to the long-term growth strategy, leveraging scale, data insights, and client relationships to lead in an evolving PBM market focused on transparency, affordability, and outcomes.

Caremark acknowledged that the traditional “market basket” structure, where client guarantees are tied to aggregated drug cost indices, has created margin exposure as shifts in drug mix and utilization have diverged from past expectations. The company noted that its mitigation efforts did not materialize as quickly as anticipated, prompting a modest miss in the third quarter and a revised guidance outlook. They emphasized that recontracting with clients over the next few years is critical to resetting this dynamic and restoring more predictable growth in its pharmacy benefit management business.

Similar to Cigna/ESI, Caremark described a clear evolution of its model focused on transparency, competition, and cost reduction for clients and members. They were a bit of a pioneer launching this last year so they feel like they have been building towards this with TrueCost and CostVantage. Key initiatives include narrowing formularies for high-cost specialty categories, such as replacing one GLP-1 drug with a lower-priced option, and expanding point-of-sale rebate programs to ensure that members pay the lowest possible price at the counter. They feel this transition is a response to the growing affordability challenges in U.S. healthcare and believe it will better align economics between care delivery, pharmacy benefit services, and member outcomes. While near-term margin pressure is expected, the long-term strategy is built on driving higher prescription volume, lowering branded medication costs, and creating a more stable and competitive platform for sustainable growth.

They clarified that the recent margin pressure within Caremark was not caused by the new TrueCost model but rather by changes in the mix of drugs dispensed under traditional rebate-based PBM contracts. In these legacy models, Caremark guarantees clients a certain level of manufacturer rebates, but when the drug mix shifts, those guarantees can become difficult to meet. During the quarter, slower-than-expected growth in GLP-1 prescriptions and unexpected shifts in the autoimmune and HIV drug categories reduced rebate volume. This shortfall put temporary pressure on margins as the company worked to recalibrate guarantees with its clients. CVS emphasized that the TrueCost model, which eliminates traditional rebates in favor of upfront pricing transparency, remains on track and is not contributing to these short-term challenges.

AI and 20 Billion Dollar Investment Consumer Experience

Similar others in the space, CVS has positioned artificial intelligence and machine learning as key parts of its strategy to create a more consumer-focused and a digitally connected healthcare experience. In the past, the company has highlighted how AI will help personalize care plans, enhance pharmacy workflows, and improve operational efficiency across its retail, insurance, and pharmacy benefit management businesses. They plan to redesign the CVS Health app which now uses AI to power search and create personalized health to-do lists, giving consumers more proactive control over their care. The management team has stated that AI will play an important role in making care more preventive, accessible,

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.