Cigna Continues to Focus on the Commercial Insurance Market/Health Services

Strong Q3 earnings 2024 for The Cigna Group

Cigna reported earnings last Thursday before the market opened, and initially, the results impressed investors—though the market's overall drop that day overshadowed the reaction. Despite that, it was a great earnings report, reaffirming Cigna as my top pick among the "Big Six Payors," thanks to its focus on the commercial insurance market and its delivery of impactful services through Evernorth. Cigna posted an impressive 30% quarter-over-quarter top-line revenue growth, nearly reaching $64 billion in Q3. This growth was largely driven by Evernorth’s robust 36% growth, and especially by ESI, which saw a staggering 50% increase as it continued to add large clients. All told, it was a strong quarter and year for David Cordani and Cigna, as they’ve transformed from an unimaginative brand to an emerging force in healthcare. Here are the highlights and insights from the 10-Q and earnings call:

Cigna

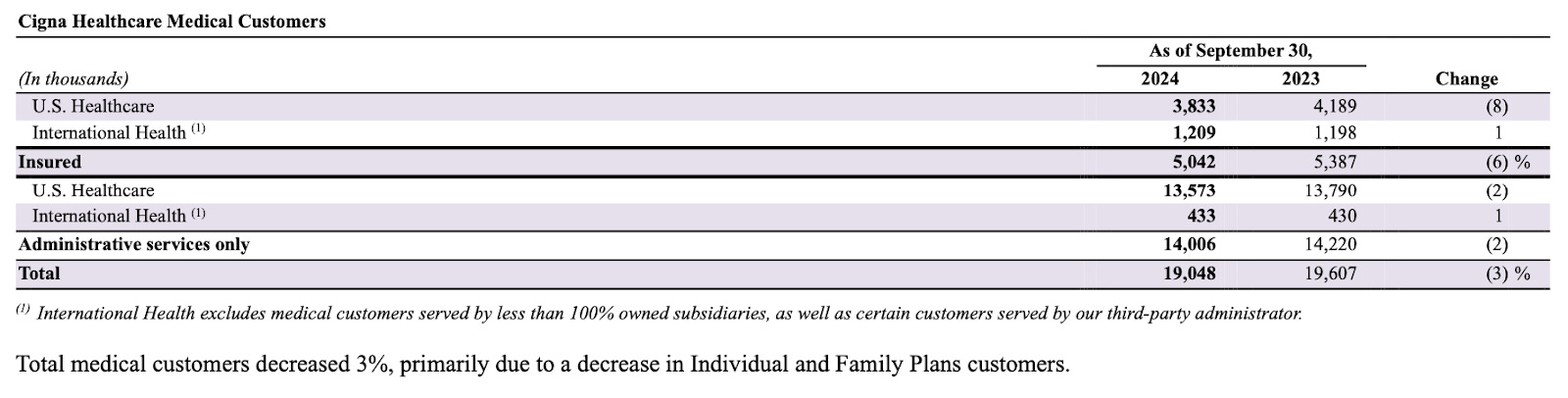

Cigna showed steady growth, with a 3% increase in top-line revenue to just over $13 billion. Like others in the industry, the health insurance segment offers consistent mid- to low-single-digit growth, while services drive revenue through innovation. Membership decreased to 19 million from 19.6 million last year, primarily due to conservative ACA pricing amid competitive pressures. Still, Cigna managed to drive higher revenue—a testament to their strategic decisions.

Commercial

Cigna focused on adding member value by expanding its network with 270,000 new providers, aiming to address the behavioral health crisis. Their goal is to provide appointments within 72 hours to avoid mental health crises, an impressive benchmark in a competitive market where UnitedHealth, the Blues, and CVS/Aetna are all vying for employers’ attention. Cigna’s commercial wins for 2025 underscore their strong positioning in the space.

Medicare Advantage Disposition

The sale of 600,000 Medicare Advantage members to HCSC remains on track to close in Q1 2025, with proceeds earmarked for share repurchases—a significant component of Cigna's recent strategy. Their ability to maintain stable STAR ratings year over year is noteworthy, especially amid industry-wide challenges. When briefly asked about the potential merger with Humana, David Cordani was quick to step away from the discussion then re-route towards capital deployment strategy.

ACA

ACA has been a growth engine, doubling in size over the past five years to over 21 million members, but increasing competition led Cigna to take a more conservative approach in last year’s bid cycle. As a result, membership declined by about 3% year-over-year, though they project 10%-15% growth in 2025. A watchpoint for ACA is the potential impact of government subsidy changes, which could affect this line’s growth trajectory.

Evernorth

Like UNH, CVS, and Elevance, much of Cigna’s growth is anticipated to come from Evernorth, their health services arm. They noted ongoing investment in specialty services, allocating $1.5 billion in capex this year to continue creating customer value

Express Scripts (ESI)

Express Scripts posted remarkable top-line growth, 50%, driven by new clients (notably Centene) and high-cost specialty drugs. In his opening remarks, David Cordani highlighted the PBM’s role in lowering drug prices, citing a University of Chicago study that demonstrated this effect over 16 months. However, the FTC’s scrutiny poses a real threat to ESI’s business in 2025/2026.

Specialty Pharmacy and Biosimilars

Specialty drugs and biosimilars are key areas of growth in healthcare services for the “Big Six Payors.” Evernorth has assembled an impressive suite of offerings—Pathwell, Accredo, CuraScript SD, and Quallent—to provide a competitive edge in the specialty and biosimilars markets, valued at an estimated $400 billion and $100 billion respectively by the decade’s end. Around 33% of Cigna members have transitioned to a $0 out-of-pocket Humira biosimilar through a partnership with Quallent, securing a portion of the $20 billion market. Here’s how these assets align:

1. Pathwell: A concierge care platform for complex and costly conditions, integrating Cigna’s network with Evernorth’s analytics and clinical expertise for personalized care.

2. Accredo: The specialty pharmacy division, focusing on medication delivery and management to support patients.

Keep reading with a 7-day free trial

Subscribe to The Healthcare Economy to keep reading this post and get 7 days of free access to the full post archives.